Friday, February 21, 2014 (Weekly Charts)

Of notable events this week was the outperformance of NASDAQ and the small caps, coupled with underperformance of the large cap stocks. NASDAQ closed at new highs, while Russell 2000 closed on a decent looking weekly candle. $SPX and $INDU dropped very slightly.

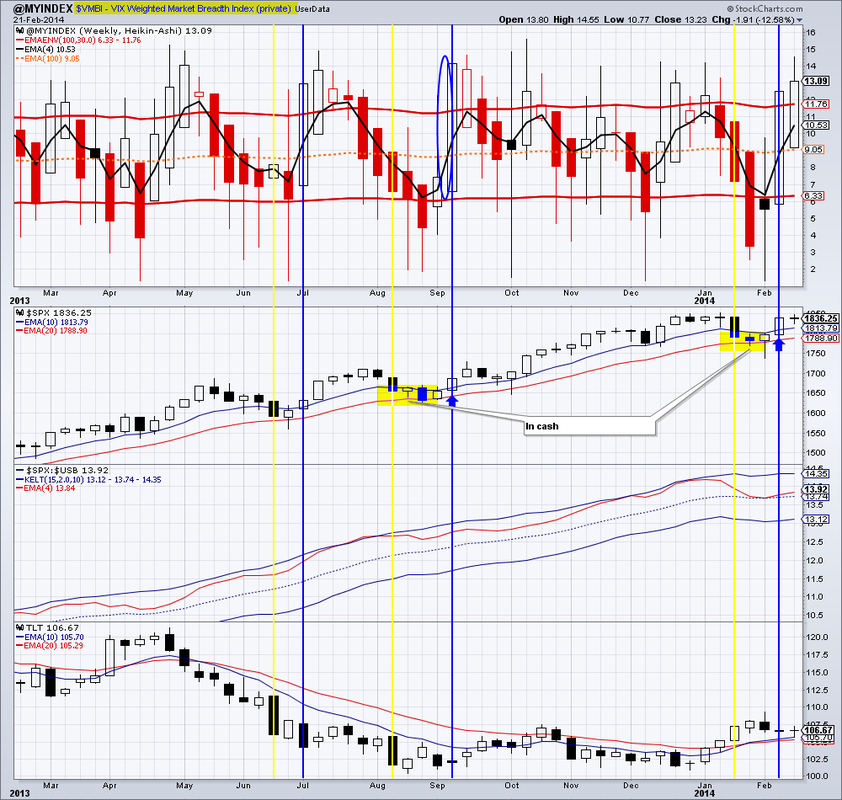

$VMBI, our in-house market breadth index, is confirming the underlying strength in this rally. Unless a complete meltdown takes place next week, we foresee continuing bullish momentum and possibly new highs for the large cap indices and the Russell.

TLT refused to go quietly and printed yet another doji hammer on the weekly chart. This reaffirms support in the $106 area. On Balance Volume is bullish, but the momentum (STO) is bearish for TLT. A decisive close below the 10 week eMA should cause selling of the long dated treasuries. Conversely, should TLT continue to at least not drop, it could weigh on the stock market. On relative basis, at this point in the game, it still makes sense to be in stocks rather then bonds since stocks are outperforming bonds.

Commodities got a strong bid last week. DBC gapped up and closed near the week's highs. Silver, natural gas, and most importantly, oil, gained. Momentum and volume patterns for DBC are bullish.

$GOLD gained slightly for the week. On the weekly gold chart, a possible Bullish flag may be unfolding. Should this pan out, then a move to around $1360 is possible shortly. Similarly, GDX, may move up to around $28.

Emerging markets underperformed $SPX again and are in danger of rolling over. EEM needs to close above $40 on the weekly charts to confirm that this rally in emerging market stocks has legs.

We are long: GDX, IYR, DEM, DVY, ETV

Of notable events this week was the outperformance of NASDAQ and the small caps, coupled with underperformance of the large cap stocks. NASDAQ closed at new highs, while Russell 2000 closed on a decent looking weekly candle. $SPX and $INDU dropped very slightly.

$VMBI, our in-house market breadth index, is confirming the underlying strength in this rally. Unless a complete meltdown takes place next week, we foresee continuing bullish momentum and possibly new highs for the large cap indices and the Russell.

TLT refused to go quietly and printed yet another doji hammer on the weekly chart. This reaffirms support in the $106 area. On Balance Volume is bullish, but the momentum (STO) is bearish for TLT. A decisive close below the 10 week eMA should cause selling of the long dated treasuries. Conversely, should TLT continue to at least not drop, it could weigh on the stock market. On relative basis, at this point in the game, it still makes sense to be in stocks rather then bonds since stocks are outperforming bonds.

Commodities got a strong bid last week. DBC gapped up and closed near the week's highs. Silver, natural gas, and most importantly, oil, gained. Momentum and volume patterns for DBC are bullish.

$GOLD gained slightly for the week. On the weekly gold chart, a possible Bullish flag may be unfolding. Should this pan out, then a move to around $1360 is possible shortly. Similarly, GDX, may move up to around $28.

Emerging markets underperformed $SPX again and are in danger of rolling over. EEM needs to close above $40 on the weekly charts to confirm that this rally in emerging market stocks has legs.

We are long: GDX, IYR, DEM, DVY, ETV

RSS Feed

RSS Feed